Definition of innovative medicine

The candidate list of innovative medicines in the Hong Kong setting was generated from horizon scanning conducted up to 31 December 2024. Only those medicines with Phase III trial evidence were considered eligible for inclusion and were subsequently included in this analysis.

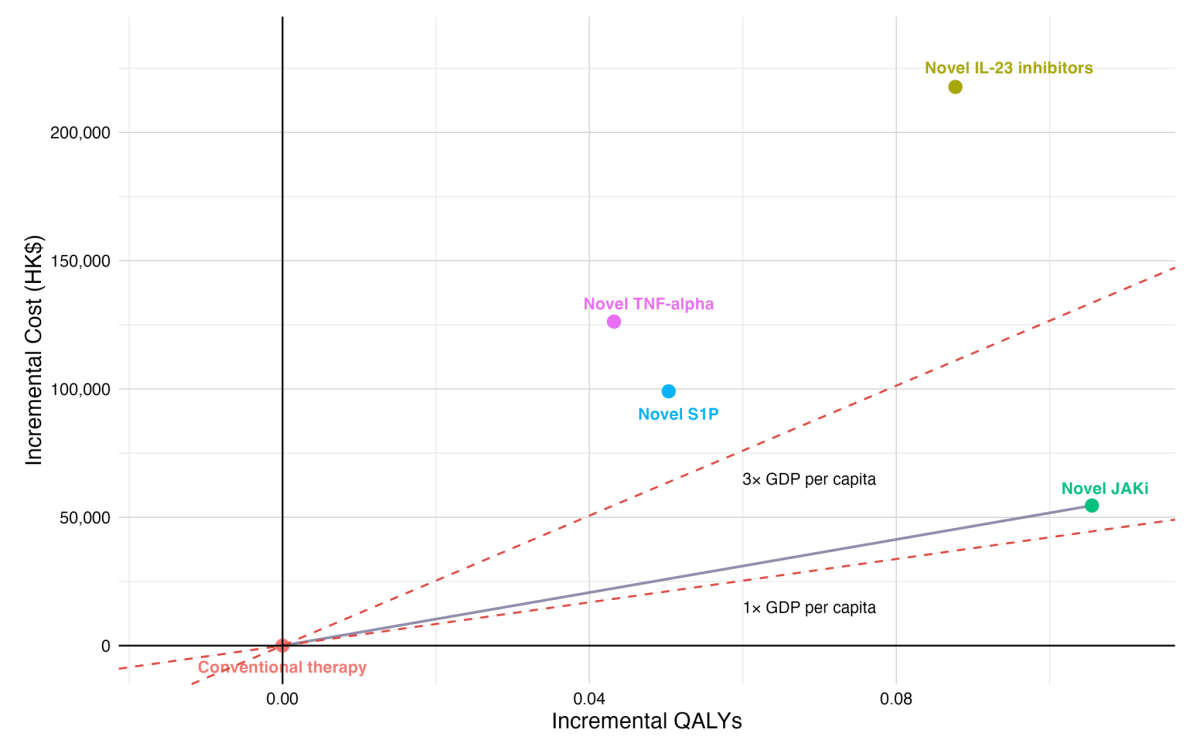

The cost-effectiveness frontier included conventional therapy and novel JAKi. This indicates that these strategies were non-dominated options in the incremental cost-effectiveness analysis. Compared with conventional therapy, novel JAKi had an ICER of HK$517,289 per QALY. This was above one times GDP per capita (HK$421,990 per QALY), but below three times GDP per capita in Hong Kong (HK$1,265,970 per QALY).

Note:

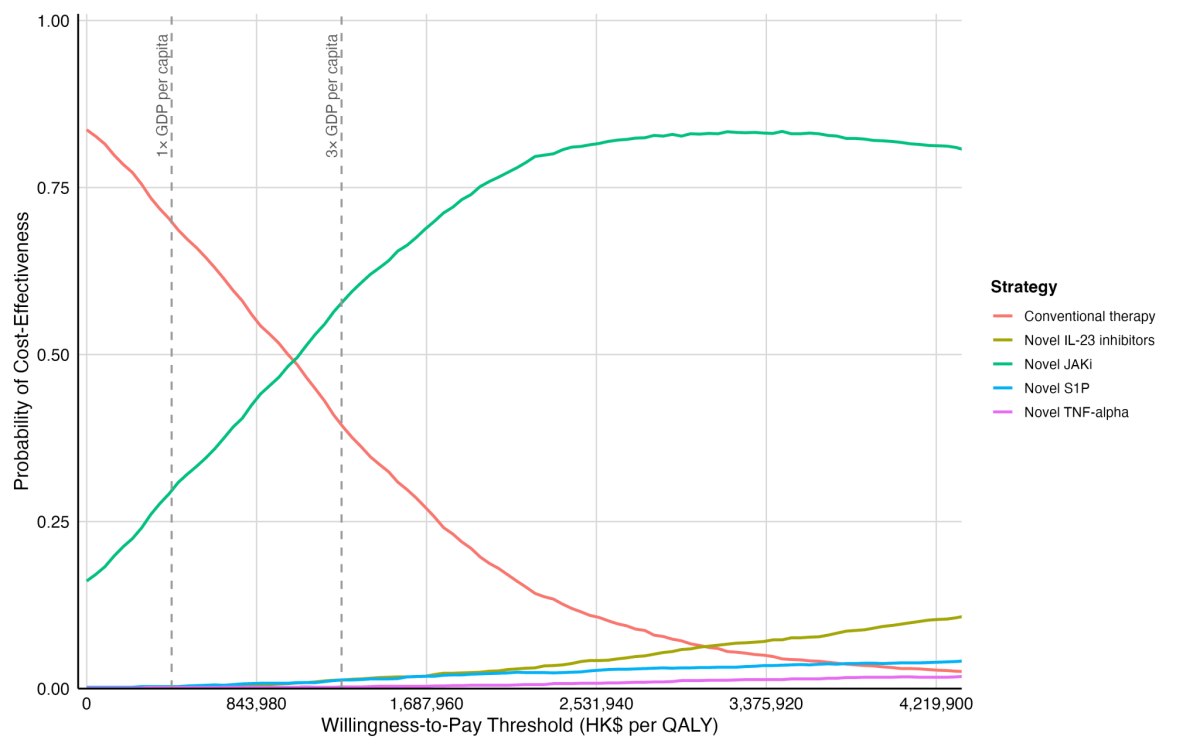

The cost-effectiveness acceptability curves summarise uncertainty in cost-effectiveness across different WTP thresholds. At the threshold of three times GDP per capita in Hong Kong (HK$1,265,970 per QALY), novel JAKi, novel IL-23, novel S1P, and novel TNF-alpha had roughly 57.7%, 0.13%, 0.13% and 0.03% probabilities of being the most cost-effective option, respectively.

Note:

Abbreviations: TNF-alpha, tumor necrosis factor-alpha antagonist; IL-23 inhibitors, interleukin-23 inhibitors; JAKi, Janus kinase inhibitor; S1P, sphingosine-1-phosphate receptor modulator; GDP, gross domestic product; QALY, quality-adjusted life year; WTP, willingness-to-pay.

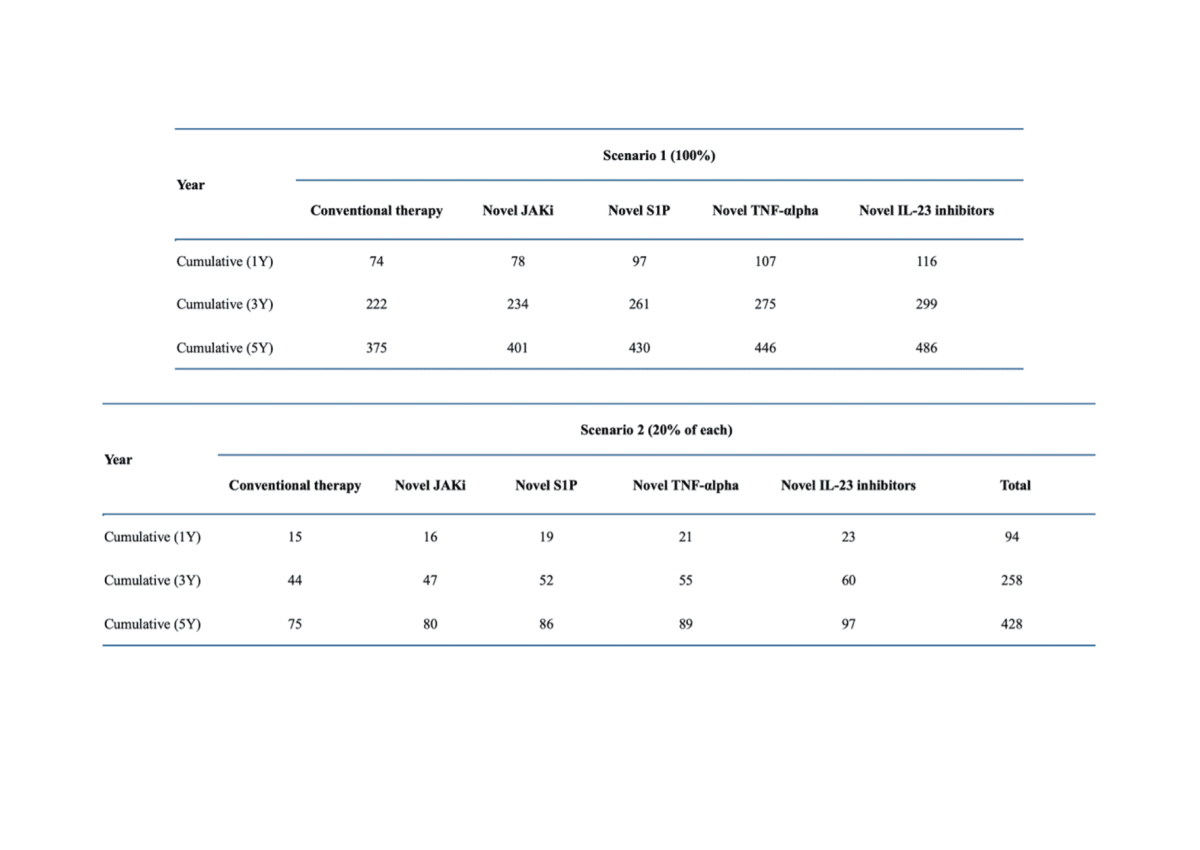

The target population comprised patients with moderate-to-severe ulcerative colitis in Hong Kong, identified from the territory-wide electronic medical database managed by Hong Kong Hospital Authority. At model entry in 2024, the baseline prevalent population was 336 patients. The annual incident cohorts entering the budget impact model in 2025–2029 were projected to be 50, 55, 58, 60, and 61, respectively.

Two market share scenarios were assessed to illustrate a range of possible uptake for each treatment strategy among patients in the treatment pathway.

• Scenario 1 (100% uptake per strategy): all entering patients were assigned to the evaluated treatment strategy from Year 1 onward.

• Scenario 2 (equal market share): entering patients were allocated according to an equal market share from Year 1 onward. For moderate-to-severe UC, this corresponded to 20% per strategy across five treatment options.

Abbreviations: UC, ulcerative colitis; TNF-alpha, tumor necrosis factor-alpha antagonist; IL-23 inhibitors, interleukin-23 inhibitors; JAKi, Janus kinase inhibitor; S1P, sphingosine-1-phosphate receptor modulator.